What is devaluation?

Quick answer: Devaluation is the drop in a car's value over time. On a lease it drives two numbers: your monthly payments (which cover the value the car loses during your years with it) and any end-of-lease recharge if the car comes back worth less than the lessor predicted -- usually because of damage or mileage beyond what they forecast.

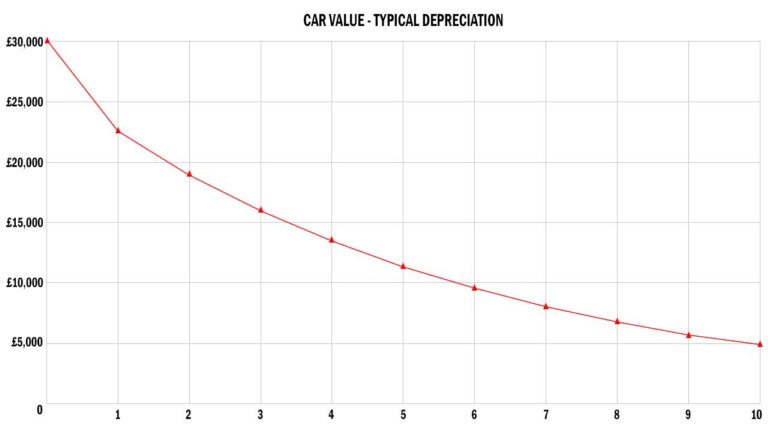

"A car halves in value the moment you drive it off the forecourt" is an exaggeration, but not by much: most cars lose close to half their showroom value in the first three years. For a lease customer, that curve is the whole story behind your monthly payment and your final bill. Understand it and most of the end-of-lease surprises stop being surprises.

How devaluation shapes a lease

A lease agreement rents you the most expensive years of a car's life. The lease company buys the car wholesale, predicts what it will be worth at the end of your contract (the residual value), and charges you the difference spread across the term, with interest and fees on top. Strip away the jargon and the arithmetic is simple: you are paying for the devaluation, plus their margin for funding it.

The curve is steep at the start and flattens later. The gap between a brand-new car and a one-year-old is huge; the gap between a three- and four-year-old is comparatively small. That is why most personal leases run two to four years: the lessor takes the fattest slice of devaluation, then sells the car on before the curve goes flat and the resale game gets harder.

It also explains something customers often find counter-intuitive: a more expensive car is not automatically a more expensive lease. What drives your monthly payment is not the sticker price but how much of its value the car is predicted to shed over your term. A car that holds its value well can lease for less per month than a cheaper car that depreciates like a stone, because the gap the payments have to cover is smaller.

Why the lease company cares so much about condition

Residual value predictions assume the car comes back in "good" condition for its age and mileage. That word does a lot of heavy lifting. Several things quietly push the real return value below the forecast:

- Higher mileage than the contracted limit

- Dents, scratches, kerbed alloys or damaged upholstery beyond fair wear and tear

- Missing items: locking wheel-nut key, service book, parcel shelf, charging cables on an EV

- A patchy or missing service history

Each of these lowers the price the car will fetch when the lessor sends it to auction. That shortfall is the extra devaluation the lease company did not bargain for, and it is exactly what the end-of-lease charges are designed to recover.

How recharges actually relate to devaluation

When you hand the car back, the lessor inspects it against the BVRLA Fair Wear and Tear guide. Damage inside the guide's threshold is absorbed as normal use. Damage outside it gets listed on an invoice as a recharge.

Here is the subtle point that catches people out. The recharge is usually presented as the cost of repair, but the repair is rarely carried out. What you are actually paying is the difference between the auction price a clean car would have fetched and the price the damaged car will fetch: the extra devaluation your car has suffered because of the damage. The wording on the invoice says "repair"; the money is really a value adjustment.

This distinction matters because it changes how you should think about pre-return repairs. A scuffed bumper corner the lessor might recharge at bodyshop rates is, to the auction buyer, simply a car that looks tired and bids lower. Tidy it before the inspection and you are not just dodging a line on the invoice; you are restoring the value that line represents.

What we see come through the workshop

The damage that triggers recharges is rarely dramatic. Tom, our operations manager, points out that the cars arriving for a pre-return tidy almost never have the kind of damage people worry about. It is the boring stuff: four kerbed alloy faces from tight Chelmsford parking, a handful of car-park door dings, a key-line down one wing, and the cluster of light scratches every car picks up from car washes and bushes over three years. Individually none of it feels like much. Lined up on a BVRLA inspection sheet, those small items add up to a recharge total that genuinely shocks people, because they had stopped noticing the damage accumulating week by week.

That is the trap with devaluation: it is gradual and invisible to the owner, then arrives all at once as a number on a final invoice.

Keeping devaluation under control

You cannot stop a car depreciating, but you can stop it depreciating faster than the lessor forecast, which is the part that costs you money. Stay inside your contracted annual mileage; excess is charged per mile from the first mile over, not from some grace band. Keep the service history complete and stamped. Gather every original item before handover: keys, the locking wheel-nut key, handbooks, charging leads, the parcel shelf. And deal with light cosmetic damage before the return rather than leaving it for the lessor's bodyshop rates.

That last point is where a SMART repair earns its keep. Localised dent, scuff and alloy work done before the inspection typically costs a fraction of the recharge the same damage would attract, because you are paying trade repair prices rather than the lessor's value-adjustment figure. The DIY version exists -- touch-up sticks, alloy kits, suction dent pullers -- but the failure modes are unforgiving on a car that is about to be inspected by a professional: a touch-up blob that catches the light, an alloy repair with a visible paint edge, or a dent puller that leaves a faint ring all read as botched repair, which an inspector can mark down harder than the original damage. The work has to be invisible to be worth doing, and invisible is the hard part.

Common misunderstandings about devaluation

"The recharge pays for a real repair." Usually not; it covers the drop in auction value the damage causes. "Minor damage will not matter." Below the BVRLA threshold it will not, but above it even small dents and scuffs get itemised. "High mileage is only a problem if I go way over." Excess mileage is charged per mile from the first mile over, with no grace band. And "servicing outside the main dealer is fine." It can be, but only if the garage uses manufacturer-approved parts and stamps the book correctly; a gap in the history is a devaluation hit at auction regardless of who caused it.

PCP and PCH: same idea, different ending

Both Personal Contract Hire (PCH) and Personal Contract Purchase (PCP) price your monthly payment off a predicted residual value, and both expect the car back in fair condition if you do not buy it. The difference is the option at the end. PCP lets you buy the car for its predicted residual, which becomes a useful lever when the market has moved: if used values have risen above the figure the lender set years ago, buying at the agreed residual and selling on can leave you ahead. PCH has no such option, so condition at return is the only number you control.

When to get an independent view

If your car has picked up visible damage and you suspect the lessor's figures will run high, an independent lease inspection before handover gives you two things: leverage to challenge an inflated recharge, and an early, honest list of what is cheap enough to put right yourself before collection. Knowing which marks fall inside the threshold and which fall outside it is the difference between spending sensibly on the items that move the auction price and wasting money tidying damage the guide would have absorbed anyway.